Mint is dead. Its replacements are ad-funded data harvesters disguised as budgeting tools. The personal finance app market had two decades to build something that actually works for the person using it, and it produced a graveyard of half-measures optimized for engagement metrics instead of financial clarity. Meridian exists because nobody else bothered to build the tool I needed — so I built it myself.

The Spreadsheet That Started It

For about three years, I tracked every dollar of my financial life in Excel. Every paycheck broken down by category. Every account balance logged monthly. Every subscription cataloged. It worked — better than any app I tried — because it forced me to understand exactly where my money went and why. The problem was the manual overhead. Updating formulas, rebuilding pivot tables, maintaining consistency across dozens of sheets. The system was sound. The medium was not.

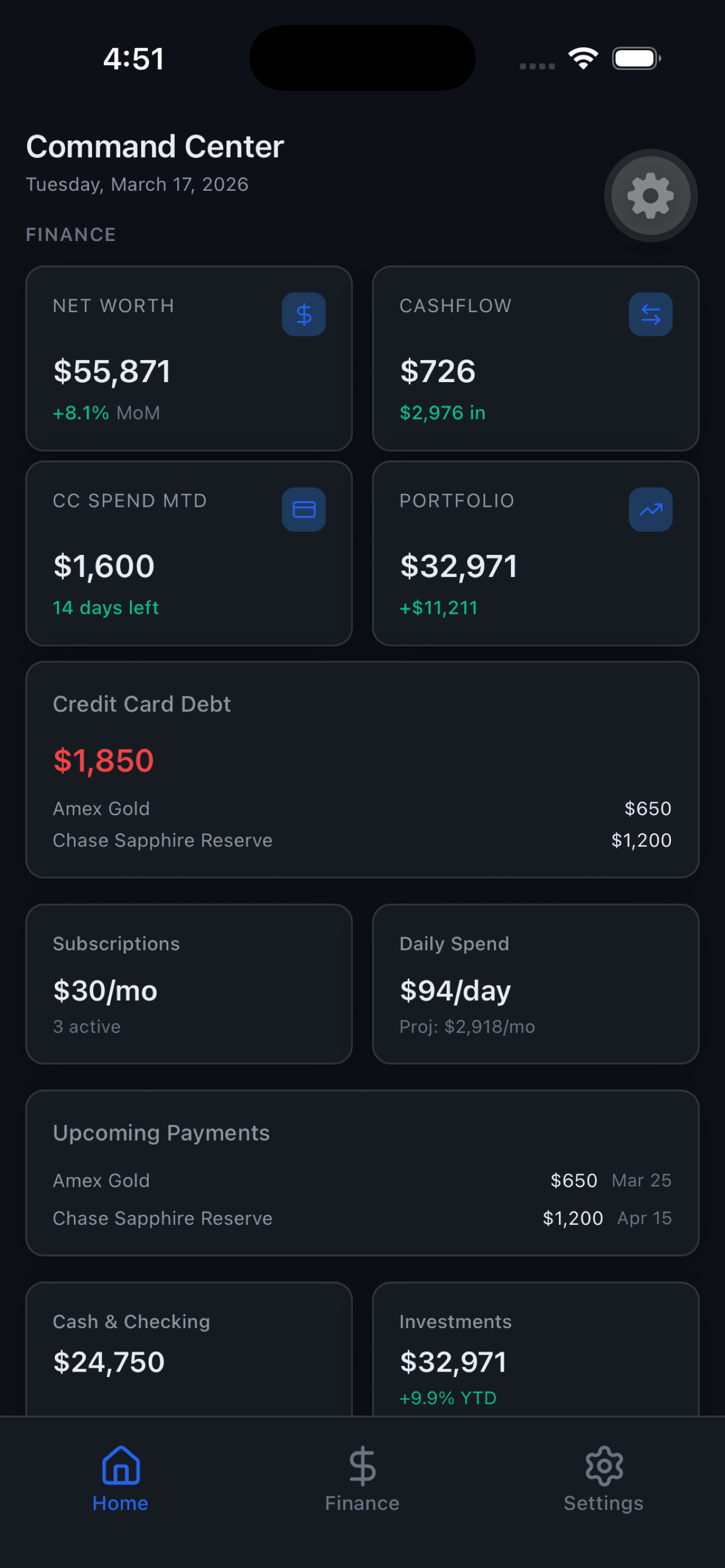

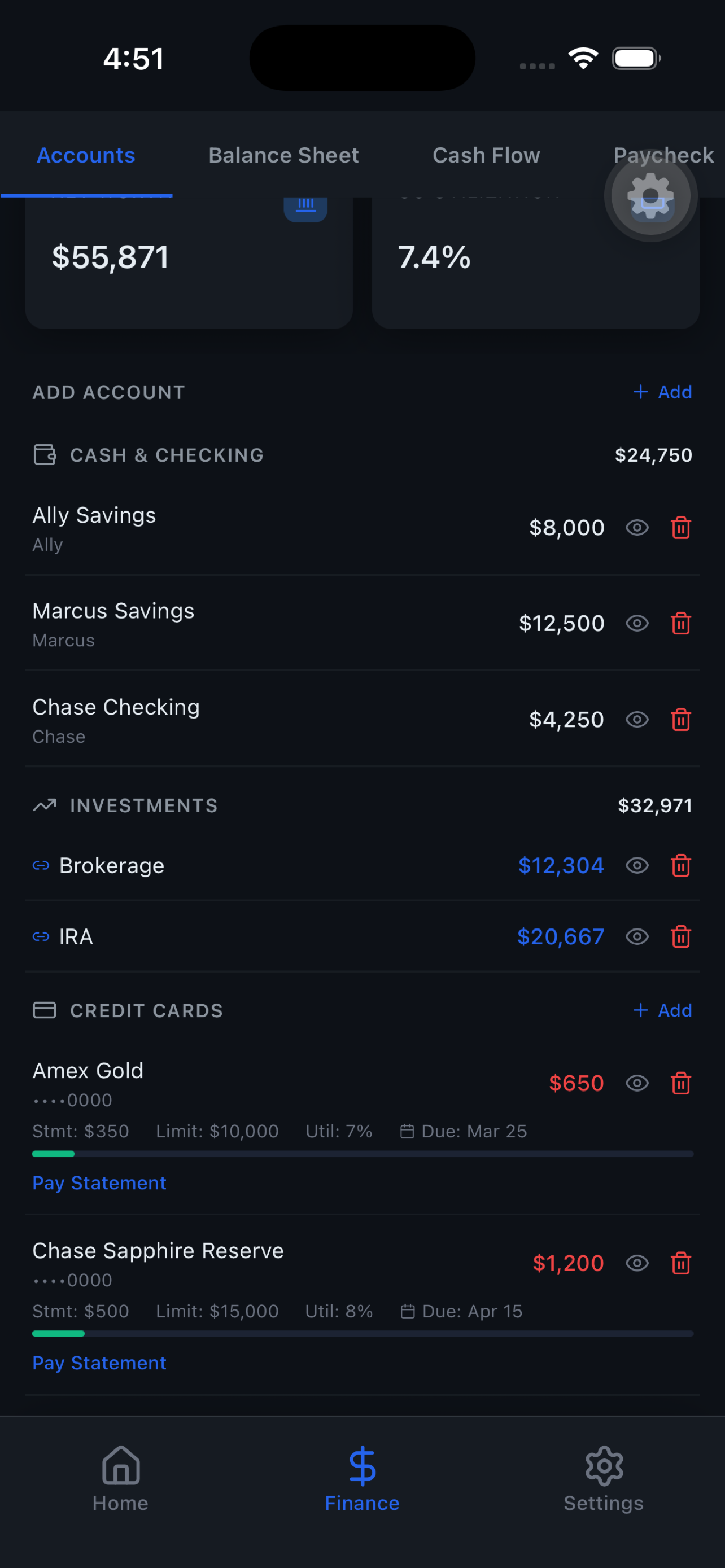

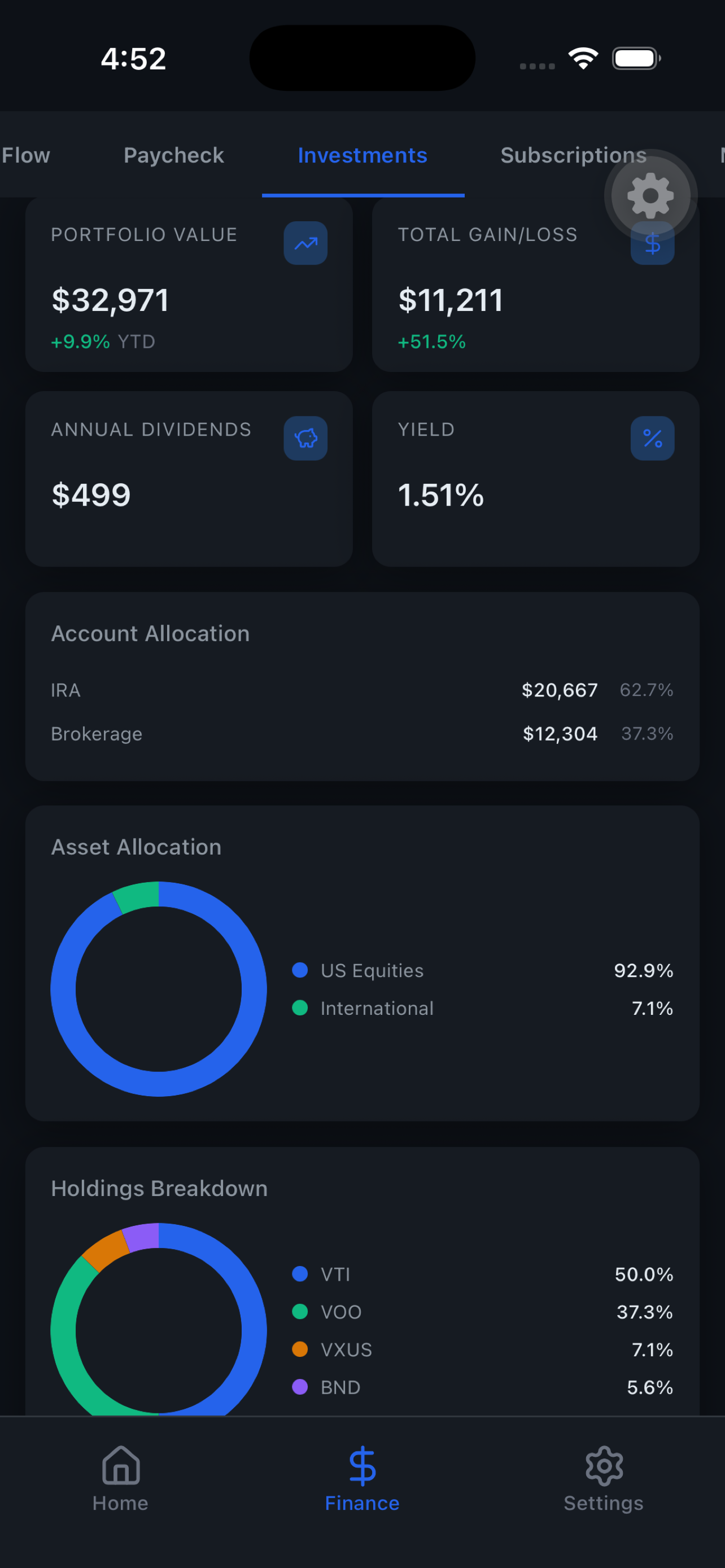

Meridian is that spreadsheet rebuilt as a real platform. A web app at meridianos.app and a native iOS app on the App Store, designed to give anyone access to the same system without the spreadsheet labor. The core data entry is manual. Everything else — the visibility, the analysis, the historical tracking — is automated.

Manual Entry Is the Point

This is the part that confuses people. Every competing app sells automation as the headline feature. Connect your bank, sync your transactions, never think about money again. The pitch sounds compelling until you understand what you are actually giving up.

Live syncing tools like Plaid record transactions on the post date, not the transaction date. That distinction matters. When your credit card posts three days after you swipe it, your spending data is systematically inaccurate. Your cash flow projections drift. Your monthly breakdowns include charges that belong to the prior period. The automation that was supposed to save you time is quietly eroding the accuracy of the data you are building your financial decisions on.

Manual entry fixes this. You enter the transaction when it happens, categorized the way you categorize it, on the date it actually occurred. It also forces something more valuable than accuracy: oversight. You should know your personal finances. Even if you are only updating once a month, the act of entering your own data keeps you connected to the reality of your spending in a way that automated syncing never will.

Automated syncing may come down the road for users who want it. But the manual-first approach is the opinionated default, and it is opinionated for good reason.

What Meridian Does Today

The platform covers the full picture of personal finance without pretending budgeting alone is enough.

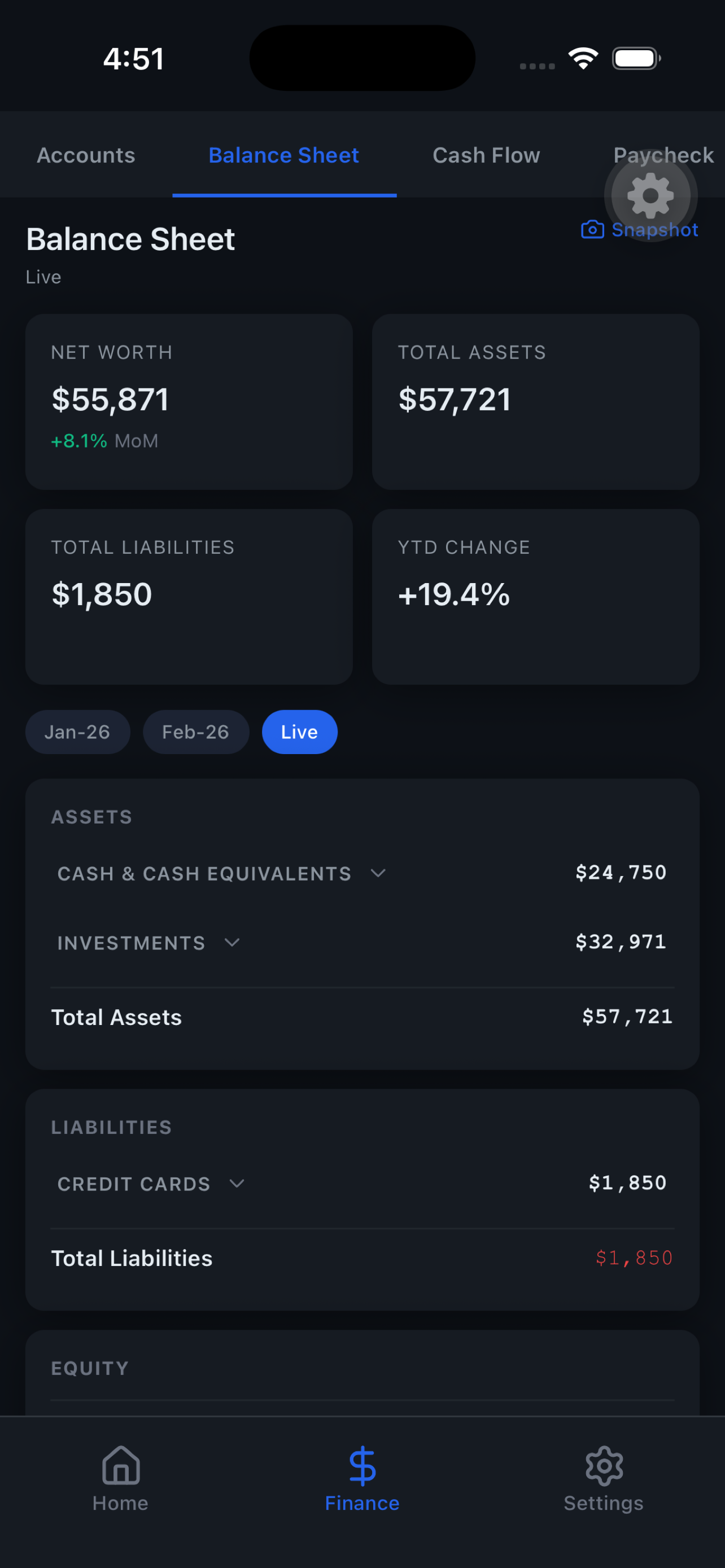

Account tracking across checking, savings, credit, and investment accounts — all in one place with historical balance data over time.

Investment portfolios with live price updates, so you can see actual portfolio performance without logging into three different brokerage apps.

A balance sheet that shows your real net worth, updated as you go, not as a once-a-year exercise.

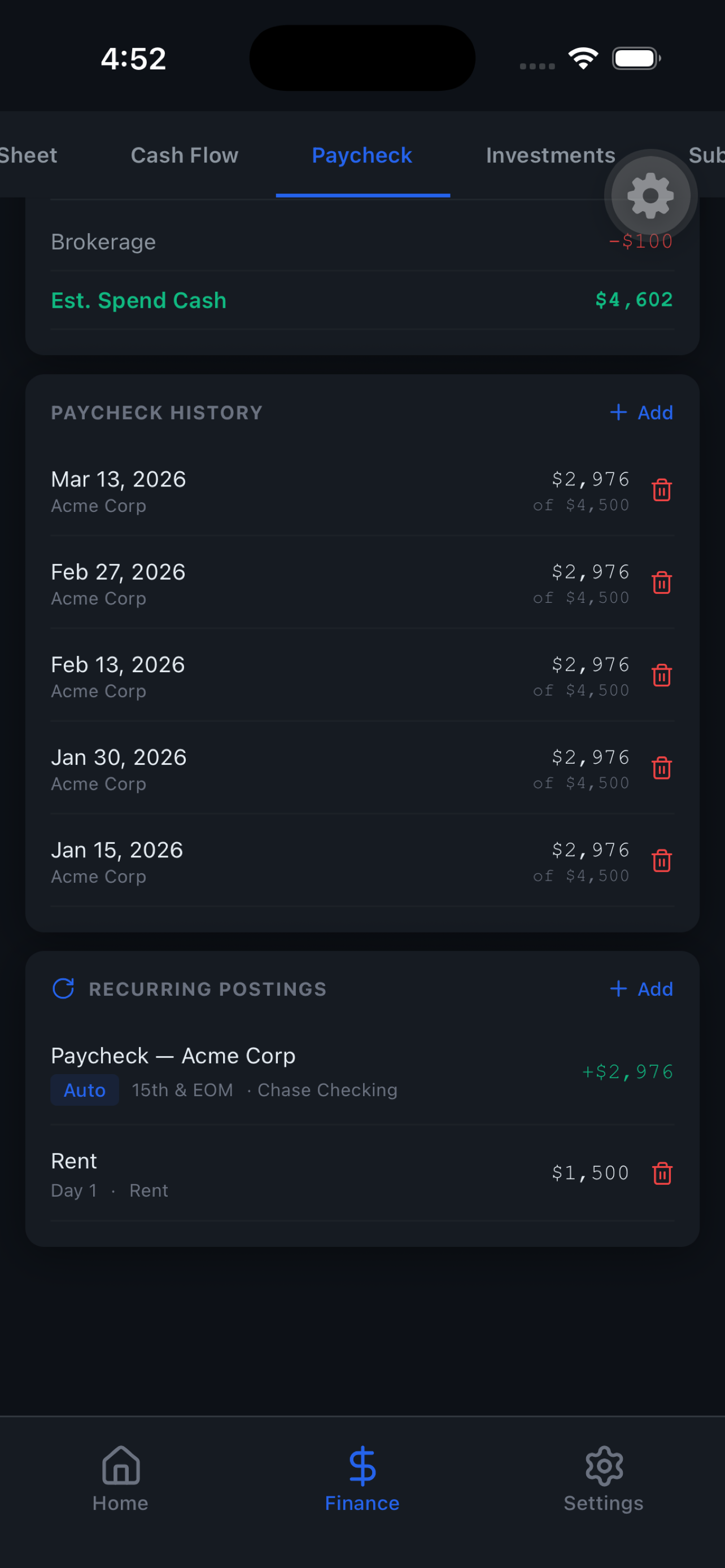

Paycheck analysis that breaks down gross-to-net so you know what you are actually keeping. Cash flow breakdowns that show you exactly where money enters and exits each month. And subscription management that surfaces the recurring charges most people forget they are paying.

None of this requires connecting a bank account. None of it sells your data. None of it shows you ads. Your data stays on the platform you control, and the platform exists to serve you — not to monetize your transaction history for credit card companies.

Why Nobody Built This

The economics explain the gap. Mint was free because Intuit monetized user data and sold financial product recommendations. Every app that followed copied the model: give away the tool, harvest the data, sell the user. The incentive structure makes it nearly impossible to build a genuinely useful finance platform inside the ad-funded model, because the product is not the app — the product is you.

Building a finance tool that refuses to monetize user data means building a tool that has to be good enough that people will actually use it on its own merits. That is a harder product problem than most teams want to solve. It is easier to build a mediocre tool with a Plaid integration and a referral program than to build something that earns daily usage through utility alone.

Meridian bets on a different model. Zero monetization of user data. Your data stays yours. The app exists because the system works — I used it for three years in a spreadsheet before writing a single line of code.

What Comes Next

Health tracking is the next major release. The same philosophy — manual-first data entry, full user ownership, no data harvesting — applied to the other domain where people desperately need a clear picture of their own data and the market keeps failing them. Personal health and personal finance share the same structural problem: the tools that exist are built to serve someone other than the person entering the data.

Meridian is live today. The web app is at meridianos.app and the iOS app is available on the App Store. If you have been looking for a finance tool that works for you instead of against you, this is it.

Further Reading

- I Will Teach You to Be Rich by Ramit Sethi — the systems-first approach to personal finance that most advice skips

- The Psychology of Money by Morgan Housel — why behavior matters more than spreadsheets, and why knowing your own data changes your behavior

- Your Money or Your Life by Vicki Robin — the original case for tracking every dollar and understanding what money actually costs you

- The Millionaire Next Door by Thomas J. Stanley — the data on what wealth actually looks like, and why visibility into your own finances is the starting point